Evolve's EASY ETF

Hello everyone, and welcome back to the blog. I’m Old Fish.

Today, we are diving deep into Evolve’s recently launched all-in-one ETF: EASY. The Ultra Yield series has been live for about six months now, and during that time, both the underlying holdings and the macro environment have shifted significantly.

In this post, I want to re-examine this product. We aren't just looking at whether the allocation makes sense on paper; we are going into the data to see how its sub-ETFs are performing in the real world.

1. Geographic & Asset Integration: The "Three-Legged Stool"

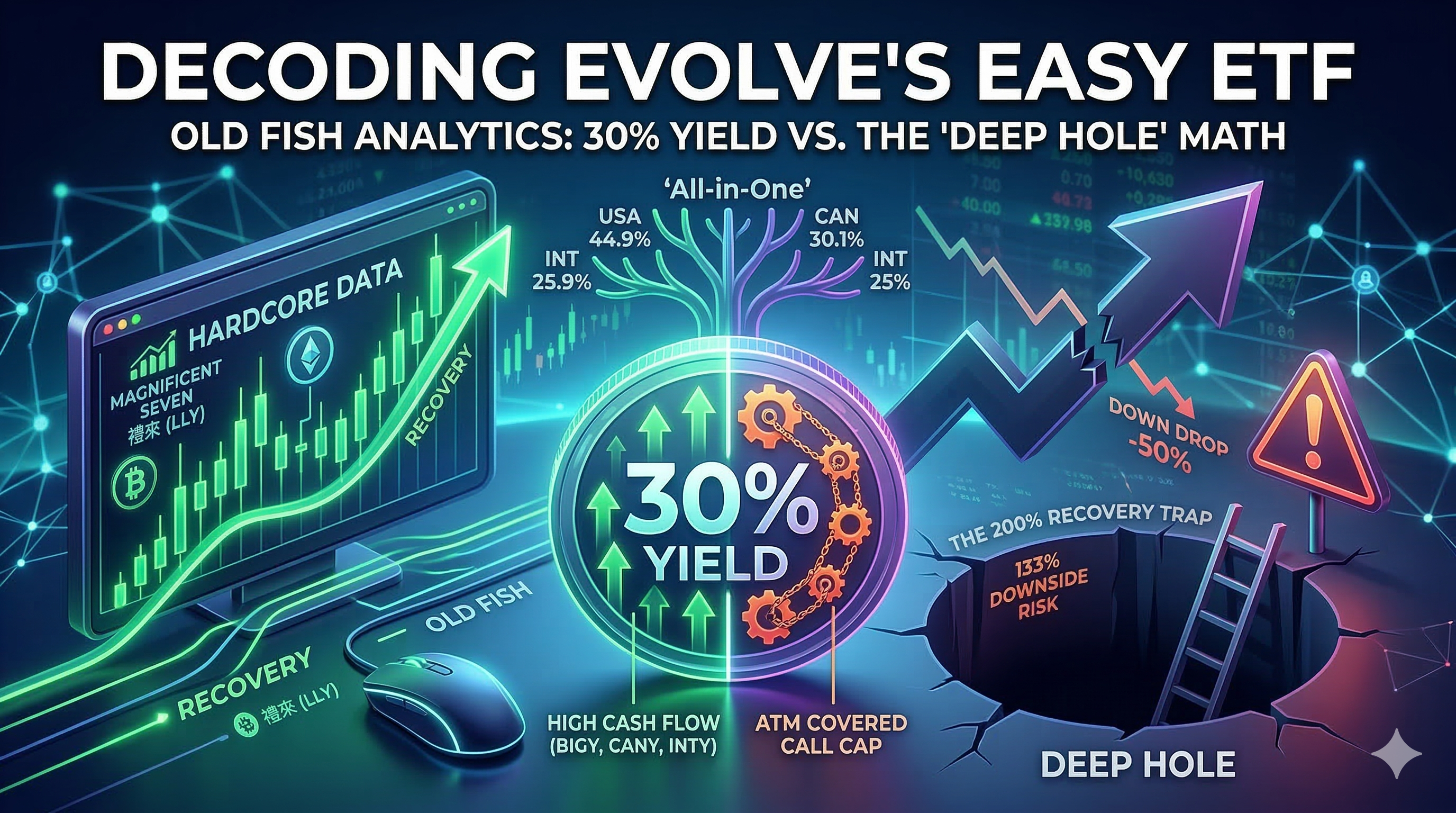

EASY’s design logic is transparent. It maps three major global markets directly to Evolve’s three core Ultra Yield tools. The allocation follows a classic global equity weight:

| Market | Weight | Underlying ETF | Key Focus |

|---|---|---|---|

| United States | 44.90% | BIGY | "Magnificent Seven," Coinbase, MicroStrategy |

| Canada | 30.10% | CANY | Domestic giants, heavy emphasis on Financials |

| International | 25.00% | INTY | Global industry leaders outside North America |

This setup is very similar to the popular XEQT—U.S. as the engine, Canada as the home bias, and International for diversification. However, that’s where the similarities end.

2. Strategy, Leverage, and that 30% Yield

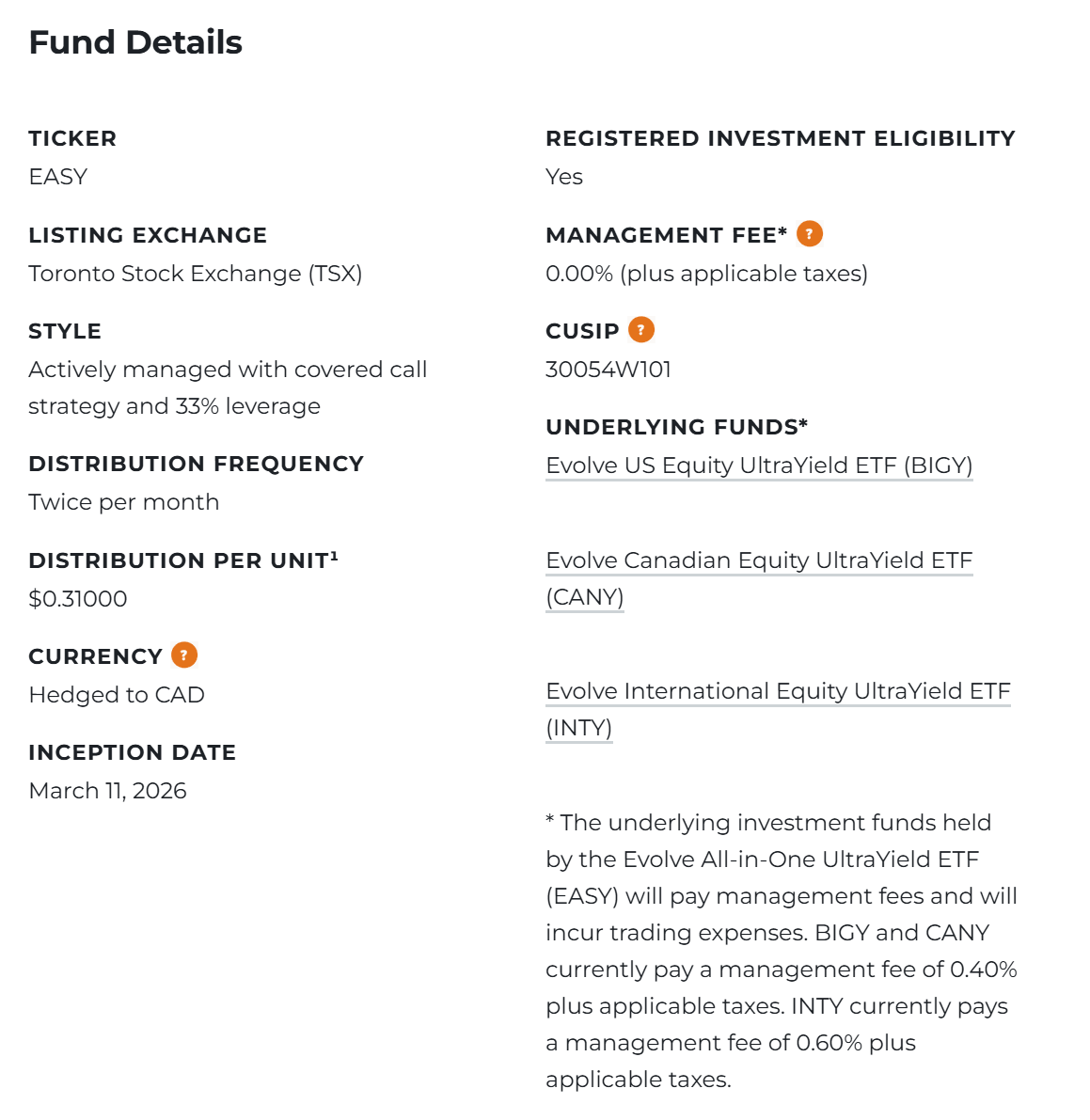

As an "all-in-one" product, EASY doesn’t charge an additional management fee (fees are collected by the underlying ETFs), which is a plus. But the real story is the strategy:

- 50% Covered Call Coverage: Specifically writing At-the-money (ATM) calls. This means the fund trades away roughly half of its potential upside in exchange for immediate cash flow.

- 33% Leverage: These ETFs use borrowed money to amplify positions.

The Result: EASY pays out twice a month with a distribution of $0.31 CAD per share. At current prices, that is a staggering ~30% Yield. It is a full pass-through strategy; Evolve is handing over every cent of the underlying dividends.

3. Hardcore Comparison: Does the Data Hold Up?

Yield is great, but total return matters more. Because these are actively managed, concentrated portfolios, we have to look at how they stack up against the competition.

BIGY vs. HHIS (U.S. Market)

Over their shared tracking period:

- Price Action: BIGY dropped -22.39%, while HHIS fell -18.52%.

- Total Return (Dividends, no reinvestment): BIGY: -7.32% | HHIS: -6.30%.

- Total Return (With reinvestment): BIGY: -8.54% | HHIS: -7.38%.

Verdict: Because BIGY employs higher leverage, it takes a much larger hit during market downturns.

CANY vs. ECHI/HHIC (Canadian Market)

The Canadian market has been relatively strong lately, but CANY's performance is... complicated:

- Price Action: CANY returned -4.98%. Meanwhile, ECHI (+13.7%) and HHIC (+10.08%) were well in the green.

- Total Return (With dividends): CANY: 5.06% | ECHI: 22.24% | HHIC: 17.62%.

Verdict: Evolve’s short-to-medium-term stock picking hasn't measured up to Ninepoint or Harvest. They need to step up their game.

4. Holdings Analysis: Shifting Gears

The latest changes in holdings show us exactly where the managers think the puck is going:

- CANY: Removed Thomson Reuters (TRI) and added Canadian Natural Resources (CNQ). This is a smart move. Given the 2026 Middle East tensions and oil volatility, they are "embracing hard assets" to hedge against geopolitical risk.

- BIGY: Added Eli Lilly (LLY) to diversify away from pure tech. However, the core remains "tech-heavy" with nearly 20% crypto exposure through MSTR and COIN. If you believe Bitcoin's rally past $70k has legs, BIGY remains an interesting play.

5. The "Deep Hole" Effect: A Sincere Risk Warning

I want to be very real with you about the risks. Evolve’s UltraYield strategy is exceptionally aggressive. Most competitors (like Global X) write Out-of-the-money (OTM) calls, leaving some room for the stock price to grow. Evolve writes At-the-money (ATM) calls. You are sacrificing almost all upside on 50% of the portfolio.

The Mathematics of a Downturn

Let’s look at a simple scenario:

- If an ETF’s NAV drops by 50%, you normally need a 100% rally to break even.

- But because the covered call strategy caps half of that upside, the underlying assets would actually need to surge 200% just for your share price to recover.

The Leverage Trap: Evolve emphasizes that you retain 66% of the upside. They rarely mention that you are facing 133% of the downside.

Final Thoughts

We are currently in a market adjustment phase. Only after weathering this storm will we see if the UltraYield series provides true value or if it's simply a high-yield trap.

If you plan to allocate to EASY:

- Strictly manage your position size.

- Utilize dividend reinvestment to average out your costs.

So, will you be buying into EASY, or are you staying on the sidelines? Let me know your thoughts in the comments below.

I’m Old Fish. Thanks for reading, and I’ll see you in the next analysis.