The Reality of Living Off Distributions

With the recent market recovery, I’m curious—have your accounts been hitting new highs?

Mine recently reached an all-time high, but looking at my current portfolio allocation, I’ve undergone a massive shift since the start of this year. I have gradually transitioned into a "Yield-focused" account. This change is driven by my current life circumstances; I am now relying on distributions to cover my daily living expenses.

Because of this, my portfolio is packed with funds that offer high payouts, even if their overall performance isn't necessarily the "best" in the market. I often wonder: if I had a larger principal to start with, would my allocation look different? Today, I want to talk about the funds that—in hindsight—really humbled me.

HDIV: The Long-Distance Champion

I recognized the quality of HDIV early on—it was actually in my very first portfolio. The reason I didn't go heavy on it later wasn't a misjudgment of its potential, but a very real-life trade-off. In a stage where I need distributions to pay the bills, HDIV's 11% yield is decent, but when faced with funds offering even more aggressive payouts (reaching towards 19%), I chose what worked best for my immediate survival.

I recognized the quality of HDIV early on—it was actually in my very first portfolio. The reason I didn't go heavy on it later wasn't a misjudgment of its potential, but a very real-life trade-off. In a stage where I need distributions to pay the bills, HDIV's 11% yield is decent, but when faced with funds offering even more aggressive payouts (reaching towards 19%), I chose what worked best for my immediate survival.

However, when you break down the mechanics behind HDIV, the structure is incredibly sophisticated. As of March 31, 2026, its sector allocation is remarkably balanced:

- Financials: 34.2%

- Energy & Gold: 16.3% and 14.7% respectively (Providing massive cash flow support and a defensive cushion)

- Utilities & Tech: 13% and 12.7%

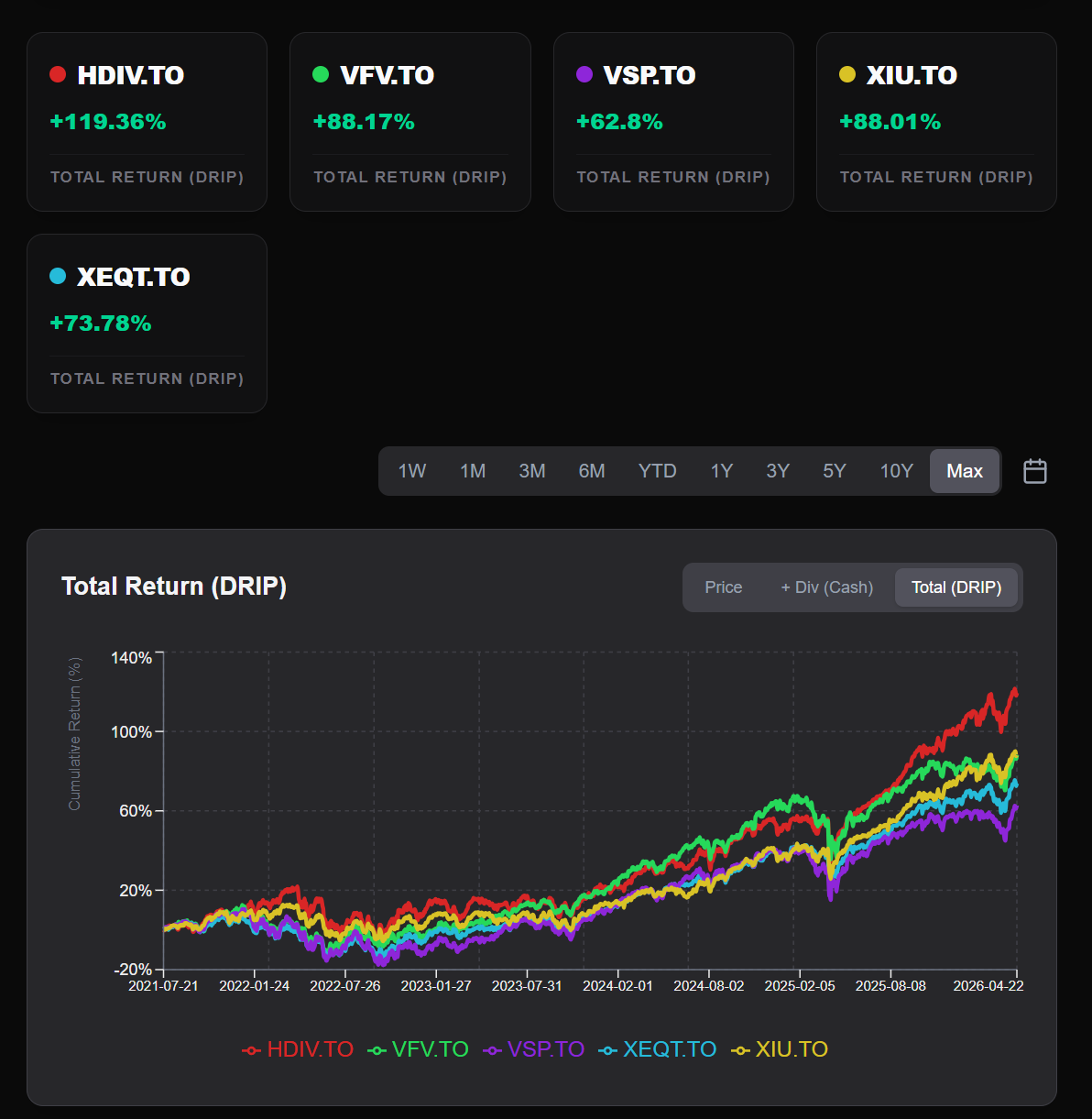

Compared to the TSX 60, HDIV holds a much higher weight in Tech and includes Gold, giving it a unique edge. The results speak for themselves: from July 2021 to April 2026, HDIV’s Total Return (DRIP) reached a staggering 119.36%.

For comparison:

- VFV (S&P 500): 88.17%

- XIU (TSX 60): 88.01%

- XEQT: 73.78%

HDIV has been the undisputed long-distance champion. Looking back, I feel a genuine sense of regret for letting it go simply because the yield "wasn't high enough" at the time.

HYLD: Evolution and Active Management

As the other core pillar of Hamilton’s income suite, HYLD has been evolving by incorporating newer funds like SDAY and QDAY. Its track record is genuinely impressive, but I originally had a nagging concern.

As the other core pillar of Hamilton’s income suite, HYLD has been evolving by incorporating newer funds like SDAY and QDAY. Its track record is genuinely impressive, but I originally had a nagging concern.

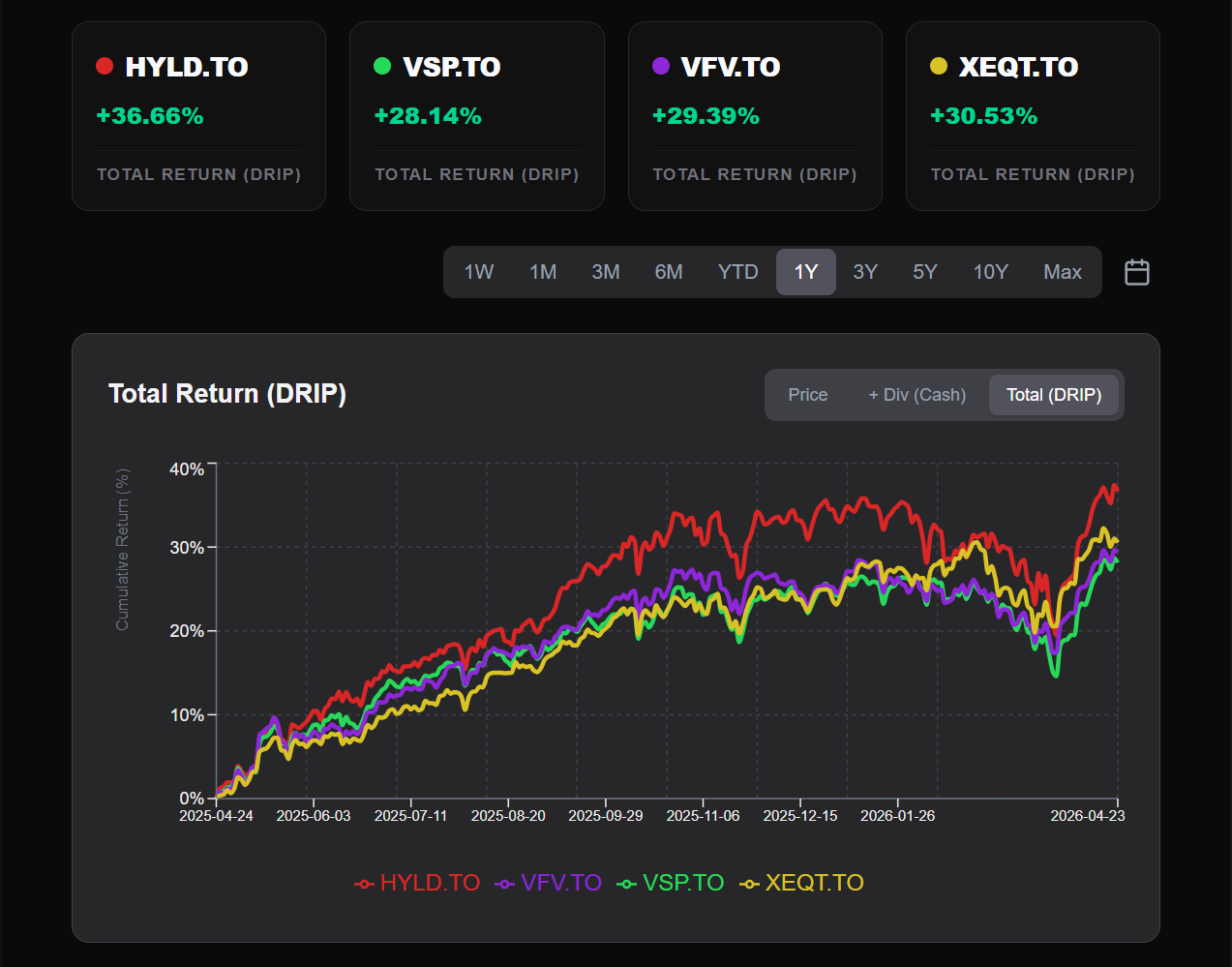

I felt like the management was intentionally "throttling" performance to make HYLD’s trajectory mirror the S&P 500 as closely as possible. Wary of that active management risk and needing higher distributions, I swapped my HYLD position for 19% yield alternatives.

In retrospect, HYLD’s performance remains stellar. Even if I’m still cautious due to my previous backtest results, a 10% to 15% allocation is perfectly reasonable. Sometimes we miss out on exceptional performers because our priorities at a specific life stage are different.

HUTE vs. UTES: Yield over Stability

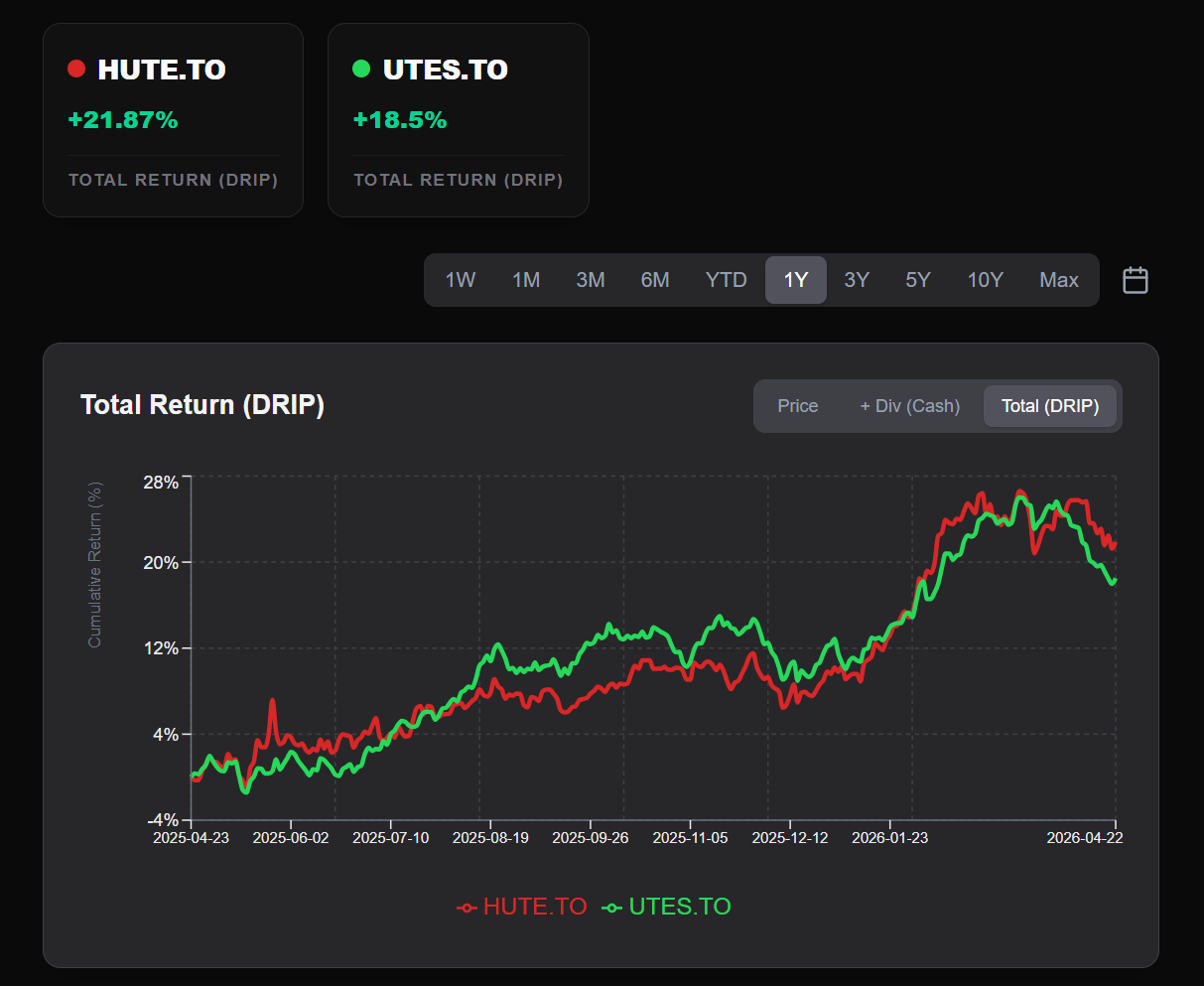

This brings me to the comparison between HUTE (Global Utilities) and UTES (Canadian Utilities). Logically, HUTE’s globally diversified, defensive profile is superior. The data supports this: over the past year (April 2025 to April 2026), HUTE returned 21.87%, while UTES returned 18.5%.

This brings me to the comparison between HUTE (Global Utilities) and UTES (Canadian Utilities). Logically, HUTE’s globally diversified, defensive profile is superior. The data supports this: over the past year (April 2025 to April 2026), HUTE returned 21.87%, while UTES returned 18.5%.

The Trade-off:

- HUTE Forward Yield: ~9.58%

- UTES Forward Yield: ~18.12%

For someone needing cash flow for immediate survival, that 18% yield was too tempting to ignore. While I technically "lost" about 3% in total return by chasing the higher yield, I don’t regret it. UTES solved my immediate cash flow crisis, and that was its true value to me.

ECHI vs. CDAY: The Growth Gap

Finally, let’s look at the defensive gap. I chose CDAY as my defensive play because its underlying asset is an index (CMVP), which felt like a safer "floor."

Finally, let’s look at the defensive gap. I chose CDAY as my defensive play because its underlying asset is an index (CMVP), which felt like a safer "floor."

But the data doesn't lie. From August 2025 to April 2026:

- CDAY Total Return: 20.54%

- ECHI Total Return: 34.76%

While I bought psychological security with CDAY, I missed out on a much more explosive growth phase with ECHI. It is a reminder that sometimes we chase "defensiveness" so hard that we lose sight of better growth vehicles.

Conclusion: Survival vs. Statistics

The common thread here is the tug-of-war between Total Return and Cash Flow. As a data-driven investor, I know the importance of total return, but when faced with real-life bills, the numbers often have to take a backseat to survival.

Seeing HDIV’s 119% return or ECHI’s explosive growth is humbling, but I don’t regret my choices. The ultimate goal of investing isn't to have a perfect backtest curve—it’s to sustain our lives. These "life trade-offs" are an essential part of the journey.

My account reaching a new high provides a chance to recalibrate. There is no "perfect" answer in investing, only the configuration that fits your current circumstances. If you're accumulating, total return is king. If you need "sustenance" to pay the mortgage and buy diapers, temporary trade-offs are a form of wisdom.

I’d love to hear from you. Over this past year, which fund has "humbled" you? Or, for the sake of immediate cash flow, what potential returns have you had to sacrifice? Let’s chat in the comments.